AR modeling

Of AR, MA, and ARMA, AR has the easiest model parameters to estimate because

approximate maximum likelihood estimates

can be obtained in closed form. MA and ARMA models generally require

an iterative approach. Thus, it makes sense to create separate methods

instead of just using ARMA functions with  .

Besides efficiency, another benefit of AR modeling is that the spectral information

can be boiled down to but a few coefficients which can hold

spectral information with high resolution.

Many natural processes such as human speech can be well modeled as an all-pole process.

As a result, we spend the most time with AR models.

AR models include linear predictive

coding (LPC), autoregressive (AR) modeling,

and reflection coefficients (RC).

Another way to represent the AR model

is using the roots of the AR polynomial.

The first

.

Besides efficiency, another benefit of AR modeling is that the spectral information

can be boiled down to but a few coefficients which can hold

spectral information with high resolution.

Many natural processes such as human speech can be well modeled as an all-pole process.

As a result, we spend the most time with AR models.

AR models include linear predictive

coding (LPC), autoregressive (AR) modeling,

and reflection coefficients (RC).

Another way to represent the AR model

is using the roots of the AR polynomial.

The first  ACF lags (

ACF lags (

) are required for a

) are required for a  -th

order AR model [31]. These ACF lags can then be transformed

to RCs or AR coefficients using invertible transformations,

thus they are equivalent from a modeling point of view.

Thus, there are four equivalent spectral representations of

an autoregressive process : AR, RC, ACF, and roots.

A good source of information on the topic is the book by

Kay [31].

-th

order AR model [31]. These ACF lags can then be transformed

to RCs or AR coefficients using invertible transformations,

thus they are equivalent from a modeling point of view.

Thus, there are four equivalent spectral representations of

an autoregressive process : AR, RC, ACF, and roots.

A good source of information on the topic is the book by

Kay [31].

Because AR features are so important in time-series analysis, they deserve

a detailed introduction.

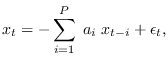

Let

, be an autoregressive process (AR) of order . This means

that

, be an autoregressive process (AR) of order . This means

that  is obtained from the recursion

is obtained from the recursion

|

(10.39) |

where

are the AR coefficients, and

are the AR coefficients, and

are independent, identically distributed

Gaussian samples of mean zero and variance

are independent, identically distributed

Gaussian samples of mean zero and variance  , known as the

innovation process. Because such a linear expansion is called a regression

in the statistics literature, and is regressed on itself, it is known

as an autoregressive process. Note that

, known as the

innovation process. Because such a linear expansion is called a regression

in the statistics literature, and is regressed on itself, it is known

as an autoregressive process. Note that  is by definition unity so it carries no

information and we often leave it out of the discussion.

An AR process may also be viewed in terms of an infinite impulse-response

(IIR) filter operating on iid samples of Gaussian noise.

From systems theory, such a process may be represented by the linear system

is by definition unity so it carries no

information and we often leave it out of the discussion.

An AR process may also be viewed in terms of an infinite impulse-response

(IIR) filter operating on iid samples of Gaussian noise.

From systems theory, such a process may be represented by the linear system

In other words, is a process with Z-transform  produced by passing the innovations

process

produced by passing the innovations

process  through a linear filter with Z-transform

through a linear filter with Z-transform

where

where

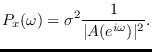

The power spectrum of the AR process is (See eq. 10.8)

|

(10.40) |

The corresponding length- circularly-stationary process has circular

power spectrum (See eq. 10.9)

circularly-stationary process has circular

power spectrum (See eq. 10.9)

|

(10.41) |

Subsections

![$\displaystyle E(z) \rightarrow \left[ \frac{1}{A(z)} \right] \rightarrow X(z).

$](img1210.png)